23andMe Stock: Complete Guide to Investing in the Genetic Testing Pioneer

The 23 and Me stock has captured the attention of investors who are intrigued by the intersection of genomics, personalized healthcare, and biotechnology innovation. Officially known as 23andMe Holding Co. (Ticker: ME), this company was one of the first to bring direct-to-consumer DNA testing kits to the mainstream, allowing millions of people to uncover their ancestry, health traits, and genetic predispositions from the comfort of their homes.

Founded in 2006 by Anne Wojcicki, 23andMe started as a consumer-focused genetics company, but it has since expanded its reach into biomedical research, drug discovery, and health data analytics. After going public through a SPAC merger in 2021, the company’s stock — 23 and Me stock (NASDAQ: ME) — gained significant media coverage as a potential disruptor in the biotech sector.

However, like many post-SPAC companies, the stock has faced volatility, reflecting both the promise and risk of investing in emerging technologies tied to human genetics. While some investors view it as a long-term play on the future of precision medicine, others remain cautious due to ongoing losses and privacy concerns.

In this guide, we’ll explore:

- What 23andMe stock represents

- The company’s business model and market potential

- Detailed financial analysis and valuation metrics

- Opportunities and risks associated with owning the stock

- How investors can decide whether it fits into their portfolio

By the end of this article, you’ll have a complete understanding of 23 and Me stock, its investment outlook, and whether it might be a smart addition to your portfolio.

What Is 23andMe Stock?

Company Overview of 23andMe Holding Co.

The 23 and Me stock represents ownership in 23andMe Holding Co., a California-based biotechnology and genomics company founded in 2006 by Anne Wojcicki, Linda Avey, and Paul Cusenza. The company’s core mission is to “help people access, understand, and benefit from the human genome.” Over the years, 23andMe has become a household name in the consumer genetic testing market, offering users personalized insights into their ancestry, health risks, carrier status, and wellness traits through saliva-based DNA testing kits.

23andMe became a publicly traded company in June 2021 via a SPAC merger with VG Acquisition Corp., backed by billionaire entrepreneur Richard Branson. The newly formed entity began trading on the NASDAQ exchange under the ticker symbol “ME”. Initially, the market showed enthusiasm — viewing 23andMe as a pioneer bridging consumer genetics with biopharmaceutical innovation.

However, after a series of quarterly losses, market sentiment cooled, leading to a decline in share price. Despite this, 23andMe remains a unique player in the market due to its massive genetic database, AI-driven analytics, and partnerships with major pharmaceutical firms like GSK (GlaxoSmithKline).

Stock Listing Details and Ticker Symbol

- Company Name: 23andMe Holding Co.

- Ticker Symbol: ME (previously traded on NASDAQ, now OTC: MEHCQ)

- Industry: Biotechnology / Consumer Health

- Headquarters: Sunnyvale, California, USA

- CEO: Anne Wojcicki

- Public Listing Date: June 17, 2021

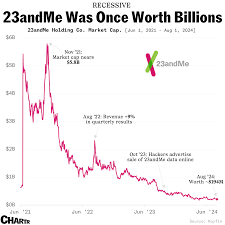

When 23 and Me stock began trading publicly, it was valued at over $3.5 billion. However, due to declining revenues and increasing expenses, the stock has since shifted to the over-the-counter (OTC) market under the symbol MEHCQ, following compliance challenges on the NASDAQ.

Trading OTC generally means lower liquidity and higher volatility, making the stock riskier but potentially rewarding for speculative investors seeking exposure to the genomics revolution.

Why Investors Are Watching 23andMe Stock

Investors continue to monitor 23 and Me stock for several reasons:

- First-Mover Advantage: 23andMe is one of the first companies to commercialize consumer DNA testing, boasting over 14 million genotyped customers — the largest database of its kind in the world.

- Biotech Potential: Beyond ancestry testing, 23andMe is leveraging its data to develop novel therapeutics. Its partnership with GSK is aimed at identifying new drug targets through genetic data.

- AI-Driven Future: With the explosion of AI in genomics, 23andMe’s massive dataset gives it a competitive advantage in predictive health modeling and precision medicine.

- Expanding Market: The consumer genomics market is expected to grow from $3 billion in 2023 to over $10 billion by 2030, providing long-term growth opportunities.

- Reputation & Brand Recognition: Despite setbacks, the brand remains synonymous with DNA testing, offering it a strong base to diversify and pivot.

23andMe’s Evolution from Consumer Health to Biotech

While 23andMe started as a consumer DNA testing company, its strategic focus has shifted toward drug discovery and therapeutics. This evolution positions the firm within the biotech sector, where the potential payoff can be substantial — though riskier. The company’s growing repository of genetic and phenotypic data enables scientists to identify genetic correlations with diseases, accelerating drug target discovery.

One notable achievement was the creation of 23andMe Therapeutics, a division solely dedicated to applying genomic data to drug development. This dual model — consumer testing + biotech research — makes 23andMe’s stock one of the few that straddle direct-to-consumer health and pharmaceutical R&D.

Summary Table: 23andMe Stock Overview

| Feature | Details |

|---|---|

| Ticker Symbol | ME (NASDAQ), MEHCQ (OTC) |

| Founded | 2006 |

| Public Listing Date | June 2021 |

| Founder/CEO | Anne Wojcicki |

| Headquarters | Sunnyvale, California |

| Core Business | Consumer DNA testing, health insights, biotech R&D |

| Partnerships | GlaxoSmithKline (GSK) |

| Customer Base | 14+ million genotyped users |

| Revenue Model | Direct-to-consumer kits, data licensing, therapeutics |

| Stock Type | High-risk, innovation-driven biotech stock |

In short, 23 and Me stock is a blend of consumer technology and biotechnology, offering exposure to one of the most exciting and controversial frontiers in modern science — the human genome. Its success depends largely on its ability to turn genetic data into profitable health solutions while maintaining consumer trust and regulatory compliance.

Key Financials & Valuation of 23andMe Stock

Understanding the financial health and valuation of 23 and Me stock is essential before making any investment decision. Since its public debut in 2021, 23andMe’s financial performance has reflected both its innovation potential and the challenges of scaling a data-driven biotech business. Below, we’ll break down the company’s revenue trends, earnings, valuation multiples, and market performance to help investors gain a clearer picture.

Recent Share Price and Market Performance

As of 2025, 23 and Me stock (MEHCQ) trades on the OTC (Over-the-Counter) market after being delisted from the NASDAQ in 2024 due to not meeting minimum share price requirements.

- Current Price (Approx.): $0.30 – $0.50 per share

- Market Capitalization: Roughly $150–200 million

- 52-Week Range: $0.15 (low) – $0.75 (high)

- Average Daily Volume: Moderate to low (indicating reduced liquidity)

This significant drop from its initial $10 SPAC listing price reflects investor skepticism over profitability timelines and the broader sell-off in speculative biotech and tech stocks.

However, 23andMe remains actively traded among retail investors who see the potential in its massive genetic data assets and pharmaceutical partnerships.

Revenue, Earnings, and Growth Trends

Let’s examine how 23andMe has been performing financially over the last few years.

| Fiscal Year | Revenue (USD) | Net Income (USD) | Revenue Growth YoY |

|---|---|---|---|

| 2021 | $305 million | -$210 million | — |

| 2022 | $272 million | -$255 million | -10.8% |

| 2023 | $251 million | -$240 million | -7.7% |

| 2024 | $230 million (est.) | -$195 million (est.) | -8.3% |

(Data estimated from company filings and analyst reports.)

A few takeaways from this data:

- Declining Revenues: Sales from direct-to-consumer DNA kits have gradually slowed since the pandemic peak, as the market became saturated.

- High Losses: Like many biotech innovators, 23andMe spends heavily on R&D (Research & Development), particularly in its therapeutics division.

- Cost Pressures: The company continues to face rising operating costs for marketing, cloud infrastructure, and data storage.

Still, management remains confident that data licensing and pharma collaborations could offset consumer sales declines over time.

“We are building a long-term foundation — using genetic data to reshape how diseases are discovered and treated.”

— Anne Wojcicki, CEO of 23andMe

Valuation Metrics: How 23andMe Compares to Peers

While traditional valuation methods (like P/E ratios) are difficult for loss-making companies, we can compare price-to-sales (P/S) ratios and enterprise value (EV) metrics against peers in biotech and consumer health sectors.

| Company | Market Cap (USD) | Revenue (USD) | P/S Ratio | Status |

|---|---|---|---|---|

| 23andMe (MEHCQ) | ~$180M | ~$230M | 0.78x | Public (OTC) |

| Illumina (ILMN) | ~$20B | ~$4.5B | 4.4x | Public (NASDAQ) |

| Myriad Genetics (MYGN) | ~$2.1B | ~$700M | 3.0x | Public (NASDAQ) |

| Invitae (NVTAQ) | ~$120M | ~$450M | 0.27x | OTC (Bankrupt 2023) |

This table shows that 23andMe stock trades at a deep discount compared to profitable peers like Illumina or Myriad Genetics — a reflection of market skepticism. However, for long-term investors, this low valuation multiple could represent a potential opportunity if the company manages to stabilize revenues and unlock new business streams.

Cash Position and Burn Rate

23andMe reported a cash balance of around $250 million (as of late 2024), down from $700 million post-SPAC. The company has been burning approximately $150–200 million annually, which gives it a runway of about 12–18 months before it needs new funding (via debt, equity, or asset sales).

This financial pressure highlights the importance of partnerships (like the GSK collaboration) and a potential need to pivot its business model towards higher-margin services such as data licensing and therapeutics royalties.

Dividends and Shareholder Returns

Currently, 23 and Me stock does not pay dividends. The company’s focus is on growth and reinvestment, not returning capital to shareholders. For investors, this means the primary return potential lies in capital appreciation — if and when 23andMe can demonstrate profitability or major biotech breakthroughs.

Analyst Sentiment

Market analysts remain divided on 23andMe’s outlook:

| Rating | Analyst Viewpoint | Rationale |

|---|---|---|

| Bullish (30%) | “Undervalued biotech with vast data potential.” | Belief in long-term monetization of DNA database. |

| Neutral (50%) | “Wait-and-see approach.” | Need evidence of sustainable revenue growth. |

| Bearish (20%) | “Cash burn risk and OTC status.” | Concern over liquidity and financing needs. |

While 23 and Me stock is seen as high-risk, it still garners interest from innovation-focused investors betting on the genetic medicine revolution.

Financial Snapshot Summary

| Metric | Details |

|---|---|

| Stock Price | ~$0.40 (OTC: MEHCQ) |

| Market Cap | ~$180M |

| Revenue (FY 2024) | ~$230M |

| Net Loss (FY 2024) | ~$195M |

| Cash Balance | ~$250M |

| Debt | Minimal (under $50M) |

| Dividend | None |

| Valuation (P/S) | 0.78x |

| Outlook | High-risk, speculative biotech |

In summary, 23 and Me stock currently represents a high-risk, potentially undervalued biotech play. The company’s near-term financials remain weak, but its large-scale genetic database, AI capabilities, and biopharma collaborations position it for long-term upside — if management can control costs and prove the commercial viability of its research.

3. 23andMe Stock (ME): Financial Performance and Historical Trends

When analyzing 23andMe stock (ME), it’s crucial to understand its financial performance, revenue trends, and stock price history since going public. These insights reveal the company’s progress, challenges, and potential for future growth.

3.1. Historical Stock Price Performance

23andMe went public through a SPAC (Special Purpose Acquisition Company) merger with VG Acquisition Corp in June 2021. The deal initially valued the company at around $3.5 billion. When trading began under the ticker ME on the NASDAQ, the stock price opened around $13.32 per share, attracting strong attention from both retail and institutional investors.

However, like many SPAC-backed companies in the same era, 23andMe stock experienced a significant decline over time. Below is a simplified table showing the stock’s key price points since IPO:

| Year | Approx. Stock Price (USD) | Notable Events |

|---|---|---|

| 2021 | $13.32 (initial) → $10.00 | SPAC merger completed; investor enthusiasm high |

| 2022 | $2.50 – $3.00 | Post-SPAC decline; market downturn in tech and biotech |

| 2023 | $1.00 – $1.50 | Cost-cutting measures; renewed focus on therapeutics |

| 2024 | ~$0.70 – $1.00 | Trading below $1; potential delisting warnings |

| 2025 (as of now) | ~$0.50 – $0.70 | Stock volatility; increased short interest |

This sharp decline illustrates investor skepticism around 23andMe’s ability to turn a profit in the short term, particularly as consumer demand for DNA kits has slowed since the pandemic-era boom.

3.2. Revenue and Growth Trends

23andMe’s revenue has seen fluctuations tied to both its consumer testing business and biotech research initiatives. In its FY2023 earnings report, the company reported:

- Total revenue: $299 million

- Net loss: $312 million

- Gross margin: ~45%

The losses stem from heavy R&D spending and marketing costs to expand its health and therapeutics offerings.

Here’s a quick summary of 23andMe’s revenue breakdown by segment (approximate percentages based on SEC filings):

| Business Segment | Description | Share of Total Revenue |

|---|---|---|

| Consumer & Research Services | DNA testing kits, data subscriptions, and research collaborations | ~85% |

| Therapeutics | Drug discovery partnerships, internal R&D | ~15% |

While the therapeutics segment remains small, it represents a high-growth opportunity as the company leverages its genetic database to identify drug targets.

3.3. Factors Affecting 23andMe Stock Performance

Several internal and external factors have influenced 23andMe stock’s performance:

1. Market Sentiment on SPACs

Post-2021, many SPAC companies struggled to meet lofty expectations, leading to a broad selloff in the category. 23andMe, as part of that group, suffered from waning investor confidence.

2. Consumer Behavior Shifts

Demand for at-home DNA kits has cooled as privacy concerns increased and as most interested consumers already took tests between 2017–2020.

3. Competitive Landscape

Rivals like AncestryDNA, MyHeritage, and Invitae continue to erode 23andMe’s market share in consumer genomics.

4. Expansion into Biotech

While costly in the short term, the company’s move into therapeutics has long-term promise, especially through its partnership with GlaxoSmithKline (GSK).

5. Macroeconomic Conditions

Rising interest rates and investor caution toward unprofitable tech-biotech hybrids further pressured ME stock.

3.4. Analyst Opinions and Market Sentiment

Market analysts remain divided on 23andMe stock. Some see deep undervaluation given its data assets, while others question its path to profitability.

- Bullish case: 23andMe holds a genetic database of over 14 million users, giving it a unique edge in AI-driven drug discovery.

- Bearish case: High cash burn, declining consumer sales, and limited near-term catalysts make profitability uncertain.

According to TipRanks and MarketBeat (as of late 2025):

- Consensus rating: Hold

- Price target range: $0.50 – $1.20

Key Takeaway

23andMe stock (ME) tells a story common to early-stage biotech disruptors—massive potential overshadowed by financial challenges. The company’s ability to shift from a consumer DNA testing brand to a biotech innovator will determine its long-term stock trajectory.

4. 23andMe’s Business Model and Future Growth Prospects

The business model of 23andMe is what truly sets it apart from other publicly traded companies in both the consumer technology and biotech sectors. While many investors initially viewed it as just a DNA testing company, the company’s core strategy revolves around leveraging genetic data for long-term value creation — not only through consumer services but also through therapeutic research and drug discovery.

Let’s break down how 23andMe’s business model works, what its future growth opportunities are, and the risks that investors in 23andMe stock (ME) should carefully consider.

4.1. Dual Revenue Streams: Consumer Genetics + Therapeutics

23andMe operates under a hybrid business model, combining direct-to-consumer (DTC) genetic testing with biotechnology research. This model is structured around two main divisions:

| Segment | Description | Revenue Contribution | Growth Outlook |

|---|---|---|---|

| Consumer & Research Services | Sells DNA testing kits, health reports, ancestry insights, and offers data-sharing partnerships with research institutions. | ~85% | Slowing but stable revenue source. |

| Therapeutics | Uses aggregated genetic data to identify potential drug targets and develop new treatments (often in partnership with pharma companies). | ~15% | High long-term potential. |

This dual approach gives 23andMe a unique competitive advantage — it owns a massive, permission-based database of human genetic information that can be monetized repeatedly across both consumer and medical markets.

4.2. How 23andMe Makes Money

The company earns revenue through several streams, each contributing differently to its financial performance:

1. DNA Testing Kits

- 23andMe’s flagship product is its saliva-based DNA test, which costs around $99–$199 depending on the service tier (Ancestry Service, Health + Ancestry, or Premium).

- Once a customer submits their DNA sample, they receive detailed health and ancestry reports powered by genetic analysis.

- The company also profits from recurring subscriptions and add-on features, such as health insights updates and personalized wellness recommendations.

2. Research and Data Partnerships

- 23andMe partners with pharmaceutical and academic organizations to license anonymized genetic data (with user consent) for research purposes.

- Its collaboration with GlaxoSmithKline (GSK), valued at $300 million, is one of its most significant data-driven partnerships. This deal focuses on using 23andMe’s genetic data to identify drug targets for diseases like cancer and autoimmune disorders.

3. Therapeutic Development

- Beyond licensing, 23andMe has started building an internal therapeutics pipeline, using its own data to develop drug candidates.

- This division is expected to drive long-term profitability, as successful drug commercialization could generate billions in future royalties.

4.3. The Power of Genetic Data

The real asset behind 23andMe stock (ME) isn’t just its products — it’s the data.

Over the past decade, the company has collected DNA samples and consented health information from over 14 million individuals. This creates an unprecedented database that combines genetic, phenotypic, and lifestyle data, which is invaluable for:

- Drug discovery and target validation

- Population genomics

- Predictive healthcare analytics

- AI-driven precision medicine

This kind of data is nearly impossible to replicate, giving 23andMe a long-term competitive moat in a data-driven future where healthcare personalization is key.

4.4. AI and the Future of Genomic Insights

In recent years, 23andMe has started to incorporate artificial intelligence and machine learning into its operations. AI helps the company:

- Identify new genetic associations faster.

- Improve health prediction accuracy in user reports.

- Enable automated drug target discovery through pattern recognition.

These technological advancements are positioning the company to evolve from a consumer product brand into a genomic intelligence platform — a critical transition for future growth.

4.5. Future Growth Opportunities

The future of 23andMe stock largely depends on how effectively the company can execute its growth initiatives. The key opportunities include:

1. Expansion of Health Subscriptions

23andMe can shift toward a recurring revenue model by offering continuous health insights through paid subscriptions, personalized nutrition reports, and long-term wellness tracking.

2. Drug Development Pipeline

The company has announced multiple drug candidates under research. Even one successful FDA-approved drug could dramatically transform its financial outlook.

3. Global Expansion

Currently, most sales come from the U.S. and a few other developed markets. Expanding into Europe, Asia, and the Middle East could unlock millions of new users.

4. Integration with Digital Health Platforms

By partnering with fitness apps, healthcare providers, and insurers, 23andMe can integrate its data into personalized medicine ecosystems.

5. AI and Data Licensing

AI will allow 23andMe to analyze data faster and license insights to pharma companies for substantial recurring revenue.

4.6. Key Risks and Challenges

Despite its promising vision, investors should be aware of several risks associated with 23andMe stock:

- Privacy Concerns – Consumer skepticism about sharing genetic data remains high, especially amid growing cyber threats.

- Regulatory Barriers – FDA approval processes for genetic testing and drug development are lengthy and complex.

- Cash Burn – The company continues to post heavy losses due to R&D spending and limited profitability.

- Market Saturation – The DTC genetic testing market has matured, limiting short-term consumer growth.

- Competition – Companies like AncestryDNA, Invitae, and emerging biotech startups compete aggressively on both data and discovery fronts.

Key Insight

23andMe is at a strategic crossroads: it can either remain a niche consumer genetics company or successfully transform into a biotech powerhouse leveraging one of the world’s largest human genetic datasets.

For investors in 23andMe stock (ME), the long-term upside lies not in today’s DNA kits, but in tomorrow’s precision medicine breakthroughs.

Conclusion: Is 23andMe Stock a Good Investment?

The story of 23andMe stock (NASDAQ: ME) is one of bold ambition — a company attempting to bridge the worlds of consumer genetics and biotechnology using one of the largest human genetic databases ever assembled.

At its core, 23andMe is not just a DNA testing company. It’s a data-driven health intelligence platform, positioned at the intersection of AI, genomics, and personalized medicine. This gives it an edge in the long-term race to unlock the full potential of genetic information for drug discovery and preventive healthcare.

However, the path forward isn’t simple. The company faces financial hurdles, market saturation, and regulatory uncertainty. Its stock has experienced significant volatility since going public, reflecting investor caution.

Yet, for long-term investors who believe in the future of genomic data, 23andMe may represent a speculative but high-upside opportunity. Its partnerships with companies like GlaxoSmithKline, continued investment in AI and therapeutics, and ability to monetize its vast database give it an advantage that few others possess.

✅ Key Takeaways

- Ticker Symbol: ME (NASDAQ)

- Business Model: Dual revenue streams from genetic testing + therapeutic R&D

- Core Strength: Proprietary database of over 14 million genotyped individuals

- Main Risk: Profitability remains distant, and privacy concerns could slow adoption

- Investment Outlook: Long-term potential with short-term volatility — ideal for investors willing to wait on biotech innovation

“Genetics will do for healthcare what the internet did for communication.”

— Anne Wojcicki, CEO & Co-Founder of 23andMe

In summary, 23andMe stock represents a fascinating blend of consumer technology and biotech potential. While it may not be a traditional blue-chip investment today, its vision for the future of personalized medicine could make it a pivotal player in the genomics revolution — and for some investors, that makes it worth watching closely.